Why 2025 Is a Turning Point for Quantum Computing

Quantum computing has spent most of its existence as a discipline of extraordinary promise and limited delivery. That balance is beginning to shift — and 2025 is the year in which the shift became difficult to dismiss.

From laboratory curiosity to geopolitical asset

Quantum information science (QIS) crossed a threshold in 2025 that separates incremental academic progress from strategic national capability. Governments are no longer treating quantum computing primarily as a research investment to be assessed over decades; they are treating it as a dual-use technology that will affect military intelligence, critical infrastructure security, and economic competitiveness within a measurable planning horizon.

The US–China tech competition, already intense across semiconductors and artificial intelligence, has acquired a quantum dimension that is qualitatively different from those earlier contests. Unlike chip fabrication — where chokepoints such as lithography equipment are relatively well understood — quantum hardware relies on a much wider set of scientific disciplines: superconducting qubit physics, cryogenic engineering, neutral-atom trapping, quantum error correction theory, and classical control electronics. Advantage is harder to measure and harder to block.

Why the 2025 milestone cluster matters more than any single announcement

Individual quantum announcements have a poor track record of meaning what headlines suggest. What makes 2025 structurally different is the convergence of several developments happening in close succession: a verified hardware record from a state research institution, a first commercial deployment from a Chinese company, and a series of policy documents that signal China is moving from capability-building to capability-deployment.

The McKinsey Quantum Technology Monitor (June 2025) described 2025 as the year in which the quantum sector globally moved from “demonstrating quantum advantage in narrow tasks” towards “identifying near-term commercial value” — a framing that applies with particular force to China, where state coordination compresses the timeline between laboratory achievement and funded deployment.

This matters for any organisation — government, financial institution, or technology company — trying to decide when to act on quantum risk and quantum opportunity. 2025 provides the clearest set of reference points yet.

China’s Key Quantum Milestones of 2025

Two systems dominate the 2025 milestone picture. They are architecturally different, serve different near-term purposes, and together illustrate the breadth of China’s quantum programme.

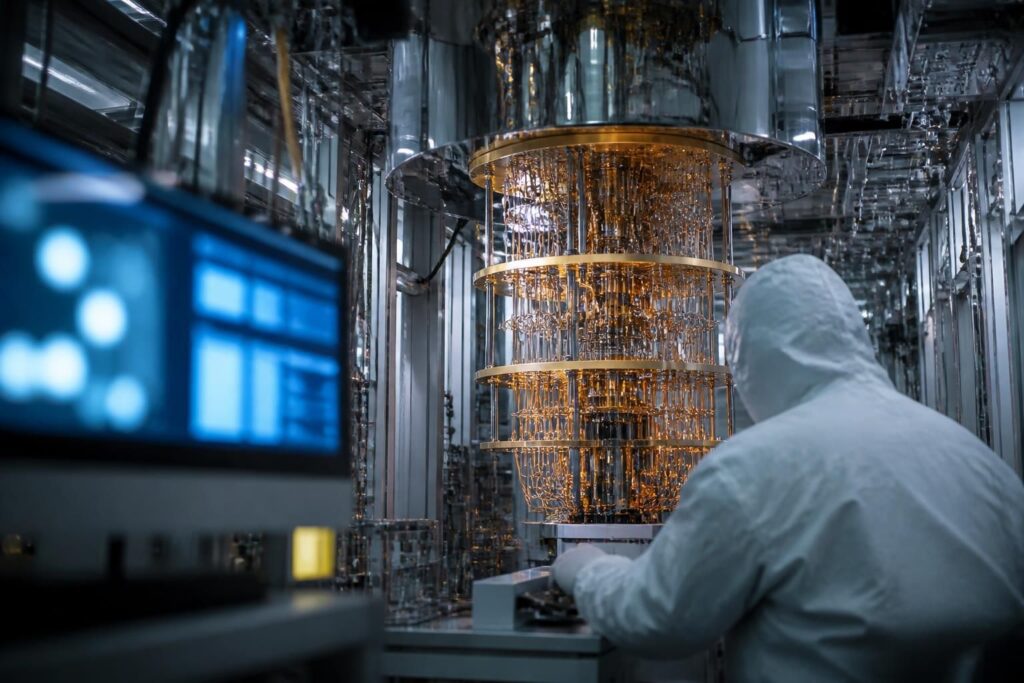

Zuchongzhi 3.0: 105 qubits and a new computational advantage record

In March 2025, the Chinese government announced the third generation of the Zuchongzhi superconducting quantum computer, developed by a team led by Pan Jianwei at the University of Science and Technology of China (USTC) in Hefei. The official specification, published on english.www.gov.cn, confirmed 105 qubits connected by 182 couplers.

The claim accompanying that announcement was specific: Zuchongzhi 3.0 completed a quantum random circuit sampling task in a time that would require the world’s most powerful classical supercomputer an estimated 6.4 billion years to replicate. That is a large number, and it deserves careful handling. Quantum random circuit sampling is a benchmark task deliberately chosen because it is hard for classical computers and tractable for quantum ones. It does not translate directly into the ability to break encryption, simulate drugs, or optimise financial portfolios. It is a proof-of-concept for quantum advantage in a narrow, well-defined problem space.

What the result does confirm is that Zuchongzhi 3.0 represents a genuine step beyond its predecessors and beyond Google’s Sycamore processor (53 qubits, 2019) in terms of qubit count. The 182 couplers — the physical connections that allow qubits to interact — are significant because entanglement between qubits is what makes quantum computation powerful; more couplers mean richer, more complex circuits. Critically, the system’s error rates and coherence times — the metrics that determine whether a superconducting quantum computer can sustain useful computation — remain the subject of ongoing measurement and peer review, and should not be conflated with the headline qubit count.

Hanyuan-1: the first commercial deployment of a neutral-atom quantum system

While Zuchongzhi 3.0 attracted the most international attention, the Hanyuan-1 system may prove more consequential for near-term applications. According to a January 2026 analysis by the Center for Strategic and International Studies (CSIS), Hanyuan-1 represents China’s first commercially deployed neutral-atom quantum computing platform — a distinction that matters because it marks the transition from laboratory demonstration to accessible service.

Neutral-atom quantum computing uses individual atoms — typically rubidium or caesium — suspended in place by laser beams (optical tweezers) as its qubits. Compared with superconducting qubits, neutral-atom systems offer several engineering advantages: atoms are naturally identical to one another (reducing fabrication variation), they can be reconfigured between computations, and they can in principle operate at room temperature rather than requiring dilution refrigerators operating near absolute zero. The tradeoffs involve gate speeds and the complexity of the optical control systems.

The commercial deployment of Hanyuan-1 — accessible to enterprise clients rather than restricted to the originating research institution — signals that China’s quantum programme is not solely pursuing record-breaking demonstrations. It is building a usable quantum computing ecosystem.

What these architectures represent technically

Both Zuchongzhi 3.0 and Hanyuan-1 operate in what the field calls the NISQ era — Noisy Intermediate-Scale Quantum. NISQ devices have enough qubits to perform computations that are difficult to simulate classically, but not enough error correction to run arbitrarily long, complex algorithms reliably. Quantum decoherence — the tendency of qubits to lose their quantum state through interaction with the environment — remains the central engineering problem.

This does not diminish the significance of what China has achieved. It contextualises it. Both machines are real, operational, and technically verified. Neither is yet a fault-tolerant quantum computer capable of the sustained, error-corrected computation that would threaten public-key cryptography or deliver transformative drug discovery results. The distance between today’s NISQ hardware and that threshold is real and measurable — and closing it is the defining race of the next decade.

How China’s Quantum Strategy Is Built: Policy, Funding, and Megaprojects

Hardware milestones do not emerge in a vacuum. Understanding China’s quantum acceleration requires understanding the policy architecture that produces it.

State coordination and the Five-Year Plan framework

Quantum technology was explicitly elevated in China’s 14th Five-Year Plan (2021–2025) as one of seven “frontier technology” priorities, placing it alongside artificial intelligence, semiconductors, and aerospace. The 15th Five-Year Plan framework, whose direction was set in 2025, continues and deepens that commitment. Unlike technology investment in most Western economies — where government funding flows through grant agencies and defence contracts at arm’s length from commercial actors — China’s Five-Year Plan framework allows the state to coordinate research institutions, state-owned enterprises, and private technology companies towards shared milestones on a defined timeline.

The US–China Economic and Security Review Commission (USCC) 2025 report, Vying for Quantum Supremacy, assessed this coordination model in detail, noting that China’s quantum megaproject funding — channelled through the National Development and Reform Commission and the Ministry of Science and Technology — has enabled sustained capital allocation to USTC Hefei and other research hubs at a scale that bypasses the annual budget uncertainty that affects US federal research programmes.

Mega-project funding vs. the US private-sector model

The contrast with the US model is instructive. American quantum computing capacity is concentrated in private companies — IBM, Google, IonQ, Quantinuum — supported by Department of Energy and DARPA grants, supplemented by the National Quantum Initiative Act (2018) and its subsequent reauthorisations. This model has produced world-class error correction research and a commercially competitive cloud quantum computing ecosystem. Its constraint is that corporate R&D timelines are driven by investor expectations, and the deepest, most foundational work — especially in fault-tolerant quantum computing — does not generate near-term revenue.

China’s state-led model has the opposite risk profile: strategic investment is insulated from quarterly earnings pressure, but accountability mechanisms are weaker and resource allocation can follow political priorities as much as scientific ones. Neither model is straightforwardly superior. The USCC report notes that China’s funded output, measured by peer-reviewed publications in quantum information science, has grown faster than any other national programme over the past decade — but that publication volume is an imperfect proxy for deployable capability.

Key institutions and research hubs driving progress

USTC Hefei, the home institution of Pan Jianwei — China’s most prominent quantum physicist and the principal architect of the Zuchongzhi programme — is the most internationally recognised node in China’s quantum network. It houses the national quantum laboratory and has produced the majority of China’s headline quantum computing results. Alongside USTC, Tsinghua University’s Institute for Interdisciplinary Information Sciences and a cluster of Shenzhen-based companies have developed parallel capabilities in quantum communications and quantum key distribution (QKD), areas where China has already deployed infrastructure at commercial scale — most notably the Beijing–Shanghai quantum-secured fibre network and the Micius quantum satellite programme. It is important to distinguish these from quantum computing: quantum communications and quantum sensing are related but separate fields with different maturity levels and different strategic implications.

The Global Quantum Race: Where the US, EU, and Others Stand

China’s progress does not occur against a static field. The quantum race involves multiple serious competitors, and the overall picture is more complex than any single ranking can capture.

US strengths: private-sector depth and error correction research

The United States retains significant structural advantages in quantum computing. IBM’s quantum roadmap has consistently delivered on its stated qubit milestones — the IBM Condor processor (1,121 qubits) and the Heron r2 architecture demonstrated in 2024 represent genuine engineering achievement, though qubit count alone is not the relevant metric. Google’s Willow chip, announced in late 2024, made a credible claim of quantum error correction below the fault-tolerance threshold for the first time — a result that, if it holds under peer review, is arguably more significant than any qubit count record, because it addresses the fundamental barrier between NISQ hardware and fault-tolerant quantum computing.

The US private sector also leads in quantum software, cloud access infrastructure, and the ecosystem of algorithm researchers who are the ultimate consumers of quantum hardware. These advantages are less visible than qubit announcements but are likely to matter more in determining who delivers practical quantum advantage first.

The error correction gap — and why it matters more than qubit counts

Logical qubits — the error-corrected, stable qubits that fault-tolerant quantum computing requires — are fundamentally different from the physical qubits counted in hardware announcements. Current estimates suggest that between 1,000 and 10,000 physical qubits are required to encode a single reliable logical qubit, depending on the error correction code used and the physical error rates of the hardware. This means that today’s 100-to-1,000 physical qubit machines, however impressive their benchmark performance, are still several engineering generations away from the logical qubit counts needed to run Shor’s algorithm at cryptographically relevant scale — the computation that would threaten current RSA and elliptic-curve encryption.

The USCC’s assessment and the broader consensus among researchers at institutions such as the MIT Center for Quantum Engineering is that the error correction gap is China’s most significant technical constraint relative to the leading US research groups. China’s hardware has scaled impressively in qubit count; the published evidence for matching progress in error correction rates is less complete.

EU, India, and other players entering the race

The EU Quantum Flagship programme, launched in 2018 with a €1 billion commitment over ten years, has produced credible results in quantum communications and quantum sensing, and is funding superconducting and photonic quantum computing research across a consortium of universities and startups. Its relative weakness compared to the US and China is in the depth of its commercial quantum computing companies and in the integration of research output into deployable systems.

India’s National Quantum Mission, approved in 2023 with a ₹6,000 crore (approximately £600 million) allocation, is the most significant new entrant to the quantum race. Its stated objectives include developing intermediate-scale quantum computers by 2026 and building a quantum-secured communications network. India’s programme is early-stage relative to the leading players but reflects a broader pattern: quantum computing is ceasing to be a US–China bilateral contest and becoming a genuinely multipolar competition. The McKinsey Quantum Technology Monitor (June 2025) identified at least fifteen national quantum programmes with meaningful funding as of mid-2025.

What China’s Quantum Advances Mean for Industries and Security

The practical stakes of this competition are not abstract. They span critical security infrastructure, pharmaceutical development, and the operational efficiency of large institutions.

Cryptography and the threat to current encryption standards

The most urgent concern associated with quantum computing progress is its eventual implication for public-key cryptography. The widely used RSA and elliptic-curve cryptography schemes depend on the computational difficulty of factoring large numbers or solving the discrete logarithm problem — tasks that a sufficiently powerful quantum computer running Shor’s algorithm could perform exponentially faster than any classical machine.

The critical qualifier is sufficiently powerful. A cryptographically relevant quantum computer (CRQC) — one capable of breaking 2048-bit RSA encryption in a practical timeframe — would require millions of error-corrected logical qubits. No such machine exists today, and no credible public roadmap places one within the next five years. What does exist, and what should concern security planners, is the “harvest now, decrypt later” threat: adversaries can record encrypted communications today and decrypt them once a CRQC becomes available. For data with a long confidentiality requirement — government communications, intellectual property, medical records — the threat is not future-dated; it is already operational.

Drug discovery, climate modelling, and financial optimisation

Beyond cryptography, quantum computing’s most discussed near-term applications involve simulation of molecular and chemical systems, where the quantum nature of the computation is a natural fit for the quantum nature of the problem. Pharmaceutical companies including Roche, AstraZeneca, and several Chinese state-affiliated research bodies have active quantum chemistry programmes aimed at accelerating drug discovery by accurately modelling protein folding and molecular interaction — tasks that classical computers handle only approximately.

Climate modelling and materials science share similar characteristics: the underlying physics is quantum mechanical, and more accurate simulation could accelerate the development of better battery materials, more efficient solar cells, and improved carbon-capture catalysts. Financial optimisation — portfolio construction, risk modelling, options pricing — is a different category of application, one where quantum speedup is plausible in the NISQ era for specific problem types, though the evidence for near-term commercial advantage here is less mature than in chemistry simulation.

Post-quantum cryptography: the defensive response

The defensive response to the quantum cryptographic threat is already underway and does not require waiting for quantum computers to arrive. The US National Institute of Standards and Technology (NIST) finalised its first set of post-quantum cryptography (PQC) standards in August 2024, after an eight-year evaluation process. The three standardised algorithms — CRYSTALS-Kyber (now ML-KEM), CRYSTALS-Dilithium (ML-DSA), and SPHINCS+ (SLH-DSA) — are designed to be secure against both classical and quantum attack, and are ready for deployment today.

The challenge is not the existence of quantum-safe encryption standards; it is the scale and complexity of the migration required to replace legacy cryptographic infrastructure across government, financial, and telecommunications systems. NIST’s guidance recommends that organisations begin cryptographic inventory and migration planning immediately, particularly for long-lived data and critical infrastructure. The fact that China’s quantum programme is advancing faster than many Western security planners anticipated makes the timeline for that migration more pressing, not less.

What to Watch in 2026 and Beyond

Predicting quantum computing timelines has a poor track record. What is possible — and more useful — is identifying the specific benchmarks that will signal genuine progression towards real-world capability.

Near-term benchmarks that will signal real-world capability

The most meaningful near-term indicator is not qubit count but demonstrated progress in quantum error correction: specifically, whether any national programme achieves logical error rates below 10−6 per gate operation at scale — the threshold at which fault-tolerant quantum computing becomes practically achievable. Google’s Willow result gestures towards this; whether it can be reproduced and extended will be a defining data point in 2025–2026.

A second indicator is commercial utility: whether any quantum computing system — Chinese, American, or European — produces a verifiable, peer-reviewed result that delivers business value beyond what is achievable classically. The McKinsey Quantum Technology Monitor identifies materials simulation and quantum chemistry as the most likely domains for an early demonstration. Announced quantum roadmaps from IBM (targeting a 100,000 physical qubit system by 2033) and from China’s national quantum laboratory provide framing for the next phase, though all such timelines should be read as aspirational.

The concept of technology decoupling — the separation of Chinese and Western quantum supply chains and research ecosystems — is also accelerating, driven by US export controls on cryogenic equipment and microwave components. This creates a risk of parallel, increasingly incompatible quantum ecosystems developing, which would slow the field overall but might accelerate certain national capabilities as domestic supply chains mature.

How Western governments and businesses should respond now

For governments, the immediate priority is cryptographic modernisation: implementing NIST PQC standards across critical systems and establishing national quantum roadmaps that are reviewed annually rather than on Five-Year Plan cycles. For businesses, the relevant actions are cryptographic inventory (understanding what data needs long-term confidentiality and how it is currently encrypted) and engagement with quantum-safe encryption vendors, most of whom can already provide migration pathways for standard protocols.

A strategic response to China’s quantum advances does not require matching China’s state investment model. It requires clarity about what Western quantum programmes are trying to achieve and on what timeline — and the institutional mechanisms to pursue those goals with the consistency that advanced technology competition demands.

Frequently Asked Questions

Which country is currently leading the quantum computing race?

No single country leads across all dimensions. China has demonstrated hardware scale and has a more coordinated state investment model; the US leads in quantum error correction research, cloud quantum computing infrastructure, and the depth of its commercial ecosystem. Google’s Willow chip and IBM’s roadmap represent the most advanced fault-tolerant research, while China’s Zuchongzhi programme holds the verified physical qubit record. The honest answer is that the race is genuinely competitive and the relevant measure — fault-tolerant logical qubits — remains out of reach for all parties.

What is Zuchongzhi 3.0 and why does it matter?

Zuchongzhi 3.0 is a 105-qubit superconducting quantum computer developed by Pan Jianwei’s team at USTC Hefei, announced in March 2025. It demonstrated quantum advantage on a quantum random circuit sampling task — completing a benchmark computation that would take the most powerful classical supercomputer an estimated billions of years to match. Its significance lies in confirming China’s ability to build and operate leading-edge superconducting quantum hardware. The benchmark task does not translate directly into cryptographic or commercial capability; error rates and coherence times remain the limiting factors.

What is the current state of quantum computing in 2025?

As of 2025, the field is firmly in the NISQ era: machines with tens to hundreds of physical qubits can demonstrate quantum advantage on narrow benchmark tasks but cannot yet run the error-corrected, fault-tolerant algorithms required for transformative real-world applications. The most significant technical frontier is quantum error correction. NIST has already published post-quantum cryptography standards in response to the eventual threat. Commercial quantum computing services are available from IBM, Google, Amazon, and now Chinese providers, but practical business advantage over classical computing remains limited to specific simulation tasks.

How does China’s quantum progress affect cybersecurity?

The principal concern is the “harvest now, decrypt later” strategy: adversaries may be storing encrypted communications now to decrypt them once a cryptographically relevant quantum computer exists. No such machine exists today, and the timeline to one is likely measured in years to decades rather than months. The practical implication is that organisations protecting long-lived sensitive data should begin migrating to NIST-standardised post-quantum cryptography now, regardless of when a CRQC arrives. China’s progress increases the urgency of that migration planning without yet constituting a direct encryption threat.