Why 2025–2026 Marks a Turning Point for Chinese Quantum Computing

From laboratory curiosity to national industrial priority

For most of the preceding decade, China’s quantum computing effort was visible mainly to specialists: a cluster of well-funded university groups, a handful of state-backed start-ups, and periodic announcements from institutions such as the University of Science and Technology of China (USTC). By the close of 2024, the field had produced credible results in quantum communications and early demonstrations in superconducting processors, but commercial deployment remained distant and the programme’s strategic weight inside the Chinese system was still contested.

That changed materially in 2025–2026. A convergence of factors — hardware milestones, a reshaping of national planning documents, and a hardening of the US-China technology rivalry — transformed quantum computing from a long-horizon research bet into a live industrial competition. Understanding why this period is different requires looking at both the technical record and the political scaffolding erected around it.

How China’s 15th Five-Year Plan elevated quantum to ‘future industry’ status

The clearest signal of political intent came on 12 March 2026, when China’s 15th Five-Year Plan (2026–2030) was formally approved. Quantum technology was listed first among seven designated “future industries” — a category distinct from the more familiar “strategic emerging industries” and carrying explicit commercialisation targets rather than merely research objectives. As specialist policy outlet PostQuantum.com noted in its April 2026 breakdown, the ordering is deliberate: placing quantum ahead of artificial intelligence, biotechnology, and advanced manufacturing signals where central planners expect the next round of transformative returns.

The plan does not guarantee outcomes. Five-Year Plans are statements of strategic intent, and China’s record of translating quantum ambitions into deployed capability has been uneven. Error rates, fault tolerance, and the distance between a headline qubit count and a practically useful machine all remain genuine engineering challenges. Nevertheless, the plan’s language commits state financing, coordinates regulatory incentives, and directs provincial governments to establish supporting industrial ecosystems — a combination that has historically accelerated Chinese technology adoption curves even when it has not delivered every promised target.

The global context: where the US, EU and China stood at the start of 2025

At the start of 2025, the quantum race had no clear, unambiguous leader — and that complexity is worth preserving rather than flattening. As the Belfer Center at Harvard Kennedy School argued in its May 2025 analysis Another Technology Race: US-China Quantum Computing, the two countries hold different advantages across different sub-domains. The United States led in superconducting processor scale and error-correction research, with IBM and Google posting the most cited fault-tolerance milestones. China led demonstrably in quantum key distribution (QKD) networks, having deployed the world’s first intercity QKD backbone, and held competitive positions in neutral-atom and photonic research.

The European Union, meanwhile, had invested substantially through its Quantum Flagship programme but struggled to translate academic strength into commercial deployments at the speed of either rival. The UK, following Brexit, pursued bilateral arrangements and channelled investment through UKRI’s National Quantum Technologies Programme — significant domestically but operating at a different scale from the US or Chinese efforts.

The net result entering 2025 was a quantum technology policy environment defined by genuine uncertainty and genuine urgency: no single actor had achieved what most physicists would recognise as fault-tolerant, general-purpose quantum computing, but the competitive dynamics meant that waiting for certainty before responding was itself a strategic choice with costs.

The 2025–2026 Quantum Milestone Timeline: Month by Month

May 2025 – US-China quantum rivalry enters a new phase

The Belfer Center’s May 2025 report marked a qualitative shift in how Western analysts framed the competition. Rather than treating Chinese quantum advances as aspirational claims requiring verification, the report’s authors — drawing on open-source technical literature and export-control filings — concluded that China had closed the gap in several hardware categories faster than consensus US government assessments had projected. Crucially, the report highlighted quantum communications as an area where China had moved from demonstration to operational infrastructure, a distinction that matters for cryptographic security planning.

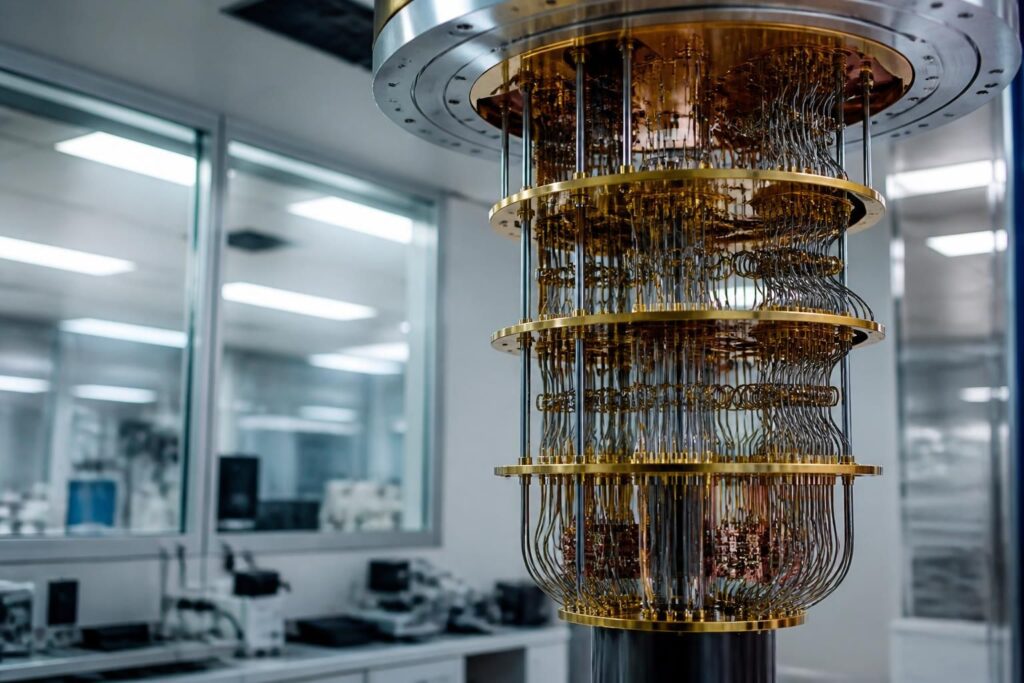

October 2025 – Hanyuan-1: China’s first commercial 100-qubit neutral-atom quantum computer

October 2025 brought the most concrete hardware milestone of the cycle: the announcement and commercial debut of Hanyuan-1, described as China’s first commercial 100-qubit neutral-atom quantum computer. The system, developed by a Beijing-based quantum technology firm with reported ties to state-funded laboratories, represented a departure from the superconducting approach that had dominated Chinese hardware development through the early 2020s.

Qubit count alone is not a reliable proxy for quantum advantage — a point the brief’s sourcing is careful to make and one the broader research community has emphasised repeatedly. What matters alongside qubit number is qubit fidelity, gate error rates, coherence times, and connectivity. The significance of Hanyuan-1 lies not primarily in its headline figure but in the modality: neutral-atom systems offer longer coherence times than many superconducting approaches and are more amenable to certain classes of error correction, though they face their own engineering challenges in gate speed and scaling. Its status as a commercial deployment — rather than a laboratory demonstration — is the detail that the McKinsey Quantum Technology Monitor would later contextualise in the broader commercialisation count.

November 2025 – USCC report flags rapid advances in quantum communications and cryptography

The U.S.-China Economic and Security Review Commission (USCC) published its annual report in November 2025, with a dedicated section titled Vying for Quantum Supremacy. The commission’s findings were notable for their institutional weight rather than their novelty: much of the technical ground had been covered in academic literature, but the USCC’s framing directed the findings at US legislators and policymakers, arguing that China’s advances in quantum communications and post-quantum cryptography represented a near-term national security consideration, not merely a long-range research competition.

The report was careful — as the brief’s avoid list suggests analysts should be — not to assert that China had achieved quantum supremacy in the sense Google’s 2019 paper popularised (demonstrating that a quantum processor could outperform a classical supercomputer on a specific, narrow task). Instead, the USCC used the phrase more loosely to describe strategic positioning, a distinction worth flagging when encountering the term in policy documents.

December 2025 – CKGSB assessment: state-driven quantum strategy reaches inflection point

The Cheung Kong Graduate School of Business (CKGSB) published an assessment in December 2025 concluding that China’s quantum programme had crossed what it described as an “inflection point” — the transition from state-funded basic research toward commercially viable applications, driven by the convergence of hardware maturity, government procurement mandates, and a growing domestic quantum software ecosystem. The CKGSB analysis noted that regional governments in provinces including Anhui, Guangdong, and Zhejiang had begun formalising procurement frameworks for quantum-secured communications infrastructure, creating early revenue streams for domestic vendors.

March 2026 – 15th Five-Year Plan approved; quantum listed first among seven future industries

As noted in the strategic framing above, 12 March 2026 was the formal approval date for the 15th Five-Year Plan. The plan’s quantum provisions extend beyond rhetorical priority: they include directives for national laboratory coordination, timelines for government adoption of quantum-secured communications, and investment targets at both central and provincial levels. PostQuantum.com’s April 2026 policy breakdown identified this as the point at which quantum computing ceased to be a discretionary research priority and became a mandatory industrial development target with accountability mechanisms attached.

April 2026 – McKinsey Quantum Technology Monitor: 30+ commercial deployments confirmed

McKinsey’s Quantum Technology Monitor, published in April 2026, provided the most comprehensive commercial snapshot of the period. The report confirmed more than 30 commercial quantum computing deployments globally, with China accounting for a material share — particularly in quantum communications infrastructure and early-stage optimisation applications in logistics and financial services. The monitor also offered market size projections that have become reference points for strategic planning discussions (addressed in the market impact section below). Importantly, the McKinsey team noted that the gap between the number of deployments and genuine quantum advantage — where quantum systems outperform the best available classical alternatives on real-world tasks — remains significant for most use cases outside narrowly defined quantum simulation.

China’s Quantum Hardware Landscape: Technologies in Play

Superconducting qubits: China’s established path and its current leaders

Superconducting quantum processors have been China’s primary hardware focus since the early 2010s, with USTC’s Zuchongzhi series producing the most internationally peer-reviewed results. Superconducting systems operate at temperatures near absolute zero, use Josephson junctions to create artificial atoms (qubits), and offer relatively fast gate operations. China’s CSIS analysis from January 2026, Understanding China’s Quest for Quantum Advancement, identified superconducting qubits as the area where China’s academic output most closely tracks US progress, though it noted that fault-tolerant operation — the threshold at which quantum error correction makes the system reliably useful — remains some distance away for both countries.

The leading Chinese institutional players in superconducting quantum computing include USTC (which produced the Zuchongzhi series), Origin Quantum (a USTC spin-out and one of China’s most commercially active quantum firms), and a cluster of hardware groups supported by the Chinese Academy of Sciences. Origin Quantum’s cloud-accessible quantum computing platform, OriginQ, represents China’s most direct equivalent to IBM Quantum’s cloud offering and has been used to build out a domestic user community.

Neutral-atom systems: why Hanyuan-1 matters beyond qubit count

Neutral-atom quantum computing uses individual atoms — typically rubidium or caesium — trapped by laser light and manipulated with additional laser pulses to create and operate qubits. The approach has attracted significant research interest because neutral atoms are inherently identical (eliminating a source of variability present in fabricated superconducting devices) and can offer longer coherence times, which gives the quantum state more time to evolve before decoherence destroys the computation.

Hanyuan-1’s commercial status is significant because neutral-atom systems have, until recently, been harder to scale and operate outside highly controlled laboratory settings than superconducting alternatives. Its October 2025 deployment suggests that Chinese engineering teams have made sufficient progress on laser control, vacuum systems, and classical control electronics to cross the commercialisation threshold — a development that mirrors progress being made simultaneously by US firms such as Atom Computing and QuEra. The qubit fidelity figures for Hanyuan-1 had not been independently verified in peer-reviewed literature at the time of writing, and that caveat matters: claimed fidelity and independently benchmarked fidelity have differed in previous Chinese hardware announcements.

Photonic and trapped-ion approaches: the diversification strategy

China’s quantum hardware landscape is not monolithic. Photonic quantum computing — which uses photons (particles of light) as qubits — is being pursued by groups at Zhejiang University and through commercial entities, offering potential advantages for room-temperature operation and integration with optical communications infrastructure. Trapped-ion systems, which use electrically charged atoms held in electromagnetic traps, are also under active development, particularly at institutions with strong atomic physics traditions.

This diversification is deliberate and reflects both the genuine scientific uncertainty about which hardware modality will achieve fault-tolerant quantum computing first and a strategic hedge against the risk that any single approach hits an insurmountable engineering wall. The CSIS January 2026 analysis noted that China’s breadth of hardware investment, while sometimes presented as evidence of inefficiency, may prove a strategic asset if the leading modality shifts — as it has done more than once already in this field’s history.

Quantum high-performance computing integration: bridging classical and quantum

One of the more practical near-term developments in China’s quantum programme is the integration of quantum processors with classical high-performance computing (HPC) infrastructure. Rather than positioning quantum computers as standalone replacements for classical systems, Chinese national laboratories and commercial partners are developing hybrid architectures in which quantum processors handle specific sub-problems — optimisation, simulation of molecular systems, sampling tasks — while classical HPC handles the surrounding computation.

This quantum HPC integration approach, sometimes described under the heading of a national quantum operating system (China quantum OS) effort, is pragmatic: it allows quantum hardware to deliver value at current fidelity levels without requiring fully fault-tolerant operation. It also, as the CKGSB December 2025 assessment noted, creates a natural procurement pathway for government and state-enterprise customers who already operate large HPC installations.

Policy Architecture: How China Funds and Organises Its Quantum Push

State investment flows: how much is China actually spending?

Precise figures for Chinese quantum investment are genuinely difficult to establish, and anyone who quotes a single authoritative number should be viewed with caution. Investment flows through multiple channels: the National Natural Science Foundation of China, the Ministry of Science and Technology’s national key R&D programmes, the Chinese Academy of Sciences institutional budget, provincial government co-investment schemes, and state-guided venture funds. PostQuantum.com’s April 2026 analysis identified what it described as an “investment gap” — the divergence between publicly announced figures (which are selective) and the full budgetary commitment when provincial and parastatal sources are included.

The most commonly cited Western reference point comes from a 2022 Georgetown CSET estimate suggesting China had committed approximately $15 billion to quantum information science, compared with roughly $3.7 billion from the US federal government over a comparable period. Both figures are likely to have grown through 2025–2026, and the US figure does not include substantial private-sector investment from IBM, Google, Microsoft, and others. The comparison is useful as a directional indicator — Chinese state investment is substantially larger on the government side — but it does not translate directly into capability, where the relationship between funding and results is non-linear.

Regional quantum ecosystems: hubs beyond Beijing

China’s quantum programme is geographically distributed in ways that are easy to miss in analyses focused solely on Beijing. Hefei, the capital of Anhui province and home to USTC, functions as the country’s primary quantum research hub, with a concentration of spin-out companies, national laboratory facilities, and the Hefei National Laboratory for Physical Sciences at the Microscale. Shanghai has developed a parallel ecosystem focused more on quantum communications and financial sector applications, supported by proximity to China’s largest financial institutions. Shenzhen and Guangzhou have attracted quantum computing investment linked to the Pearl River Delta’s electronics manufacturing base, where the supply chain for cryogenic components and precision optics has a natural home.

This regional quantum ecosystem structure has parallels in US quantum hubs (Chicago Quantum Exchange, Silicon Valley photonics clusters) and mirrors the European Quantum Flagship’s node-based organisation. Its practical significance is that disrupting or sanctioning any single institution or company will have limited impact on the overall programme — a consideration that has informed US export control strategy discussions, as noted in the USCC November 2025 report.

Open-source quantum software: China’s emerging strategy

An underreported dimension of China’s quantum programme is its growing investment in quantum software infrastructure. Origin Quantum’s isQ quantum programming framework and the development of Chinese-language quantum development environments represent efforts to build a domestic developer community that does not depend on US-controlled platforms such as IBM’s Qiskit or Google’s Cirq. The related search interest in “China quantum open-source” and “China quantum OS” reflects genuine curiosity about whether China is pursuing software-layer sovereignty analogous to its efforts in operating systems and database software for classical computing.

The honest assessment is that Chinese quantum software is currently less mature and less internationally adopted than US alternatives, and that the research community — including Chinese researchers — continues to rely heavily on Qiskit and its ecosystem. However, the strategic direction is clear, and the 15th Five-Year Plan’s emphasis on full-stack quantum capability (hardware through software through applications) suggests this gap will receive targeted attention through 2030.

The role of universities and national laboratories

China’s university sector plays a structurally different role in quantum development than its US counterpart. Where US university quantum groups primarily feed talent and fundamental research into an ecosystem dominated by private companies, Chinese universities — particularly USTC, Tsinghua, and Peking University — maintain direct relationships with national laboratory facilities, receive direct state funding for applied research, and are expected to produce both intellectual property and commercially deployable systems. The national laboratory system, anchored by the Hefei National Laboratory and the Beijing National Laboratory for Condensed Matter Physics, provides a coordination layer that has no precise Western equivalent.

This integration of academic, governmental, and commercial actors is both a strength and a potential rigidity: it accelerates technology transfer from laboratory to application, but it can also create dependencies on state procurement priorities that distort technology choices away from what the market might independently select.

Security Implications: Cryptography, PQC and the ‘Store Now, Decrypt Later’ Threat

What quantum supremacy means for current encryption standards

The security implications of quantum computing advances are real, but the timeline is frequently misrepresented in both directions — either dismissed as science fiction or presented as an imminent catastrophe. A properly calibrated assessment requires distinguishing between what current quantum hardware can do and what a future, large-scale, fault-tolerant quantum computer could theoretically do.

Current quantum processors — including Hanyuan-1 and the most advanced US systems — cannot break RSA, elliptic curve cryptography, or AES encryption. Doing so for practically relevant key sizes would require millions of logical qubits with very low error rates, sustained over long periods. Today’s systems operate with hundreds to low thousands of physical qubits, with error rates that require significant overhead for error correction. The path from today’s hardware to cryptographically relevant quantum computers is real but involves engineering challenges that have no guaranteed resolution timeline. Responsible estimates from NIST, CISA, and independent academic researchers suggest the threat to current asymmetric encryption could materialise anywhere from the early 2030s to the 2040s, with genuine uncertainty across that range.

Post-quantum cryptography: where China and the West are diverging

The Western response to the quantum cryptographic threat has been anchored in the NIST Post-Quantum Cryptography (PQC) standardisation process, which finalised its first three standards in August 2024: CRYSTALS-Kyber (now ML-KEM) for key encapsulation, CRYSTALS-Dilithium (ML-DSA) and SPHINCS+ (SLH-DSA) for digital signatures. These algorithms are designed to be secure against both classical and quantum attacks, and NIST has published detailed migration guidance for organisations.

China has not adopted the NIST PQC standards, which is not surprising given the broader context of US-China technology competition, but it is strategically significant. China’s cryptographic standards body (the State Cryptography Administration) has been developing its own post-quantum candidates, with SM-series algorithms forming part of the domestic cryptographic architecture. The divergence means that systems relying on Chinese cryptographic standards and those relying on NIST PQC standards will not be interoperable in a post-quantum world without explicit translation layers — a fragmentation of global cryptographic infrastructure with implications for international commerce, diplomacy, and intelligence.

The ‘Store Now, Decrypt Later’ risk: practical timeline for organisations

The most pressing near-term security concern is not that quantum computers will break encryption tomorrow, but that adversaries with the resources and motivation to do so may already be harvesting encrypted data with the intention of decrypting it once a sufficiently powerful quantum computer exists. This is the “Store Now, Decrypt Later” (SNDL) attack strategy, sometimes referenced under the term Q-Day — the hypothetical future date at which a cryptographically relevant quantum computer becomes operational.

The USCC’s November 2025 report flagged SNDL as an active concern in the context of Chinese intelligence collection, noting that the long shelf life of sensitive government communications, personal health records, financial data, and intellectual property makes them viable targets for collection today even if decryption lies years away. For organisations holding data that must remain confidential for a decade or more — defence contractors, pharmaceutical companies, financial institutions, critical national infrastructure operators — SNDL represents a threat that arrives before Q-Day, not after it.

The practical implication is that PQC migration cannot wait until quantum computers are demonstrably capable of breaking current encryption. Migration needs to begin now, particularly for high-value, long-retention data and the communications channels that protect it.

Quantum communications and the sovereign network agenda

China’s quantum communications programme — built around quantum key distribution (QKD) — is the dimension of its quantum programme that has advanced furthest toward operational deployment. QKD uses quantum mechanical properties to distribute cryptographic keys in a manner that is theoretically impossible to intercept without detection, offering a different approach to the post-quantum security problem than algorithmic PQC.

China has deployed the world’s most extensive QKD network, including the Beijing-Shanghai backbone and satellite-based QKD demonstrated through the Micius satellite. The USCC report and the CSIS January 2026 analysis both note that China is actively extending this infrastructure and has framed a sovereign quantum communications network as a national security asset — one that would, in principle, provide communications security even in a post-Q-Day environment without depending on cryptographic algorithms whose security rests on unproven mathematical hardness assumptions.

Western governments have been more cautious about QKD deployment, partly due to practical concerns about cost, range limitations, and the need for trusted relay nodes, and partly because NIST and the UK’s National Cyber Security Centre (NCSC) have both expressed a preference for algorithmic PQC as the primary mitigation. The divergence in approach is another dimension of the broader fragmentation of global digital security infrastructure.

Global Market Impact: What China’s Quantum Progress Means for Tech Competition

Quantum computing market size projections to 2030 and 2040

Market size projections for quantum computing should always be read with their source and methodology in mind. The McKinsey Quantum Technology Monitor (April 2026) — the most recent comprehensive market analysis available at the time of writing — projects the global quantum computing market could reach $45–$131 billion by 2040, depending on the pace of hardware maturation and the breadth of application adoption. Near-term figures are more modest: the same monitor suggests a market of $2–$13 billion by 2030, reflecting the reality that commercially viable quantum advantage remains limited to a small number of use cases in the near term.

The wide ranges in these projections are not analyst imprecision but an honest reflection of the technology’s development uncertainty. The quantum market size in 2030 will depend critically on whether error-corrected quantum processors achieve meaningful advantage in drug discovery simulation, financial optimisation, or materials modelling within this decade — an outcome that leading researchers consider possible but not certain. Treating the upper bound of these ranges as a baseline for strategic planning would be a mistake; the lower bound is equally plausible.

Industry verticals in the crosshairs: pharma, finance, climate modelling, logistics

The McKinsey Monitor and the CSIS analysis both identify four industry verticals as the most likely first beneficiaries of genuine quantum advantage:

- Pharmaceutical drug discovery: Quantum simulation of molecular interactions could dramatically accelerate the identification of drug candidates, reducing the cost and time of early-stage discovery. This application is frequently cited as the clearest near-term case for quantum advantage because the underlying computational problem — simulating quantum systems — is naturally suited to quantum hardware.

- Financial services simulation: Portfolio optimisation, risk modelling, and derivatives pricing involve combinatorial problems that are computationally expensive for classical systems and potentially tractable for quantum alternatives. Chinese state banks and investment institutions are active in early-stage quantum finance research.

- Climate modelling and materials science: Simulating new materials for batteries, solar cells, and carbon capture — applications with direct relevance to energy transition policy — represents another domain where quantum simulation could outperform classical approaches before general-purpose fault-tolerant computing is available.

- Logistics and supply chain optimisation: Vehicle routing, supply chain scheduling, and network flow problems are combinatorial optimisation challenges where quantum approximate optimisation algorithms (QAOA) may deliver early advantage, though the evidence for this at practical scale remains contested.

China’s strategic interest in all four verticals is direct: pharmaceutical self-sufficiency, financial resilience, energy security, and logistics infrastructure are all explicit priorities in the 15th Five-Year Plan and preceding policy documents.

How Western tech companies and governments are responding

The US private sector response to China’s quantum advances has been substantial. IBM’s roadmap targets fault-tolerant quantum computing through its modular quantum systems approach; Google’s Willow processor, announced in late 2024, demonstrated significant progress in quantum error correction below threshold — a landmark result that drew wide attention. Microsoft has pursued a topological qubit approach that, if successful, could offer hardware-efficient error correction. These efforts represent private capital investment at a scale that supplements US government funding significantly.

At the government level, the US has responded with export controls on advanced quantum computing components — including dilution refrigerators, specialised electronics, and certain software — though the effectiveness of these controls is debated given the international nature of quantum supply chains. The UK government’s National Quantum Strategy, published in 2023 and funded at £2.5 billion over ten years, represents a serious commitment but operates at a different scale from the US or Chinese programmes. The EU’s Quantum Flagship continues to fund research across member states, with commercial translation remaining the acknowledged gap.

Where the quantum market share battle stands today

Summarising where quantum market share stands in mid-2026 requires resisting false precision. In cloud-accessible quantum computing services, US providers (IBM Quantum, AWS Braket, Azure Quantum, Google Cloud) dominate international access. In QKD and quantum communications infrastructure, China is the clear operational leader. In the emerging market for quantum-safe security products, the US and European cybersecurity industry holds the commercial advantage, with Chinese vendors focused primarily on the domestic market. In the fundamental research that will determine long-term hardware leadership, the gap is genuinely uncertain and contested — with leading independent analysts, including those at the Belfer Center, cautioning against confident assertions in either direction.

What Should Organisations and Policymakers Do Now?

Immediate steps for technology leaders: crypto-agility and PQC migration

The most actionable response to the quantum security landscape is not to wait for Q-Day but to begin building crypto-agility into technology infrastructure now. Crypto-agility is the organisational and technical capacity to swap cryptographic algorithms without rebuilding entire systems — a capability that becomes essential both for responding to the eventual quantum threat and for keeping pace with the iterative updates to PQC standards that NIST has signalled will continue.

Concrete first steps for technology leaders include:

- Conducting a cryptographic inventory to identify all systems relying on RSA, ECC, or Diffie-Hellman key exchange — the asymmetric algorithms most vulnerable to quantum attack.

- Prioritising PQC migration for systems handling long-retention sensitive data, where SNDL risk is highest today.

- Adopting the NIST PQC standards (ML-KEM, ML-DSA, SLH-DSA) as the baseline for new system procurement.

- Engaging with supply chain and software vendors to establish their PQC migration timelines and avoid creating dependencies on quantum-vulnerable components.

- Beginning internal awareness and training programmes so that security architects and procurement teams understand the PQC transition requirements.

How UK and European organisations should interpret China’s Five-Year Plan

For UK and European organisations, the 15th Five-Year Plan’s quantum provisions carry several practical implications. First, Chinese vendors operating in quantum-adjacent sectors — telecommunications infrastructure, cloud services, advanced components — will receive state support to develop quantum-secured offerings, potentially creating pricing dynamics that challenge Western competitors in third markets. Second, the plan’s emphasis on full-stack quantum capability, from hardware to software to applications, signals that Chinese firms are building toward competitive positions across the entire quantum value chain, not merely in hardware.

UK policymakers should recognise that the NCSC’s existing guidance on quantum-safe cryptography is the correct technical direction, but that the pace of PQC adoption across critical national infrastructure and the supply chain needs to accelerate. The UK’s National Quantum Strategy provides a framework; the question is whether implementation is proceeding at a speed commensurate with the external competitive and security environment.

European organisations should additionally note that the EU’s divergence from both NIST PQC standards (which it has largely endorsed) and Chinese alternatives creates both a clarity (align with NIST) and a complexity (prepare for interactions with systems using incompatible standards in third-party contexts).

Monitoring indicators: the milestones to watch in 2026–2027

The milestones most worth tracking through 2026–2027 include:

- Peer-reviewed publication of Hanyuan-1 benchmarks: Independent verification of qubit fidelity and error rates would significantly sharpen the assessment of China’s neutral-atom progress.

- US and Chinese export control developments: Both the breadth of US quantum export controls and China’s responses (including potential restrictions on rare earth materials used in quantum hardware) will shape the competitive landscape.

- Quantum error correction milestones: Progress toward fault-tolerant operation — where logical error rates fall below physical error rates at scale — will be the most significant technical indicator of when cryptographically relevant quantum computing might arrive.

- Commercial quantum deployment counts: McKinsey’s next Quantum Technology Monitor update will indicate whether the 30+ deployment figure from April 2026 reflects a trend inflection or a plateau.

- NIST PQC adoption rates: The speed at which major technology vendors and critical infrastructure operators adopt ML-KEM and related standards will determine the West’s quantum readiness posture.

Frequently Asked Questions about China’s Quantum Computing Advances

Is China ahead of the US in quantum computing?

The answer depends on which dimension of quantum computing is being measured. In quantum communications and QKD network deployment, China is unambiguously the operational leader, having built the world’s most extensive QKD infrastructure. In superconducting quantum processor research, the US holds an edge in the most advanced fault-tolerance demonstrations, with Google’s Willow processor and IBM’s roadmap representing the current frontier. In neutral-atom computing, both countries have active programmes and the competitive position is closely contested. Treating China as uniformly “ahead” or “behind” obscures more than it reveals; the Belfer Center’s May 2025 analysis provides the most balanced multi-dimensional assessment available from an independent institutional source.

What is Hanyuan-1 and why does it matter?

Hanyuan-1 is China’s first commercially deployed neutral-atom quantum computer, announced in October